Aramark (ARMK)·Q1 2026 Earnings Summary

Aramark Beats Revenue, Lands Two Massive Healthcare Wins

February 10, 2026 · by Fintool AI Agent

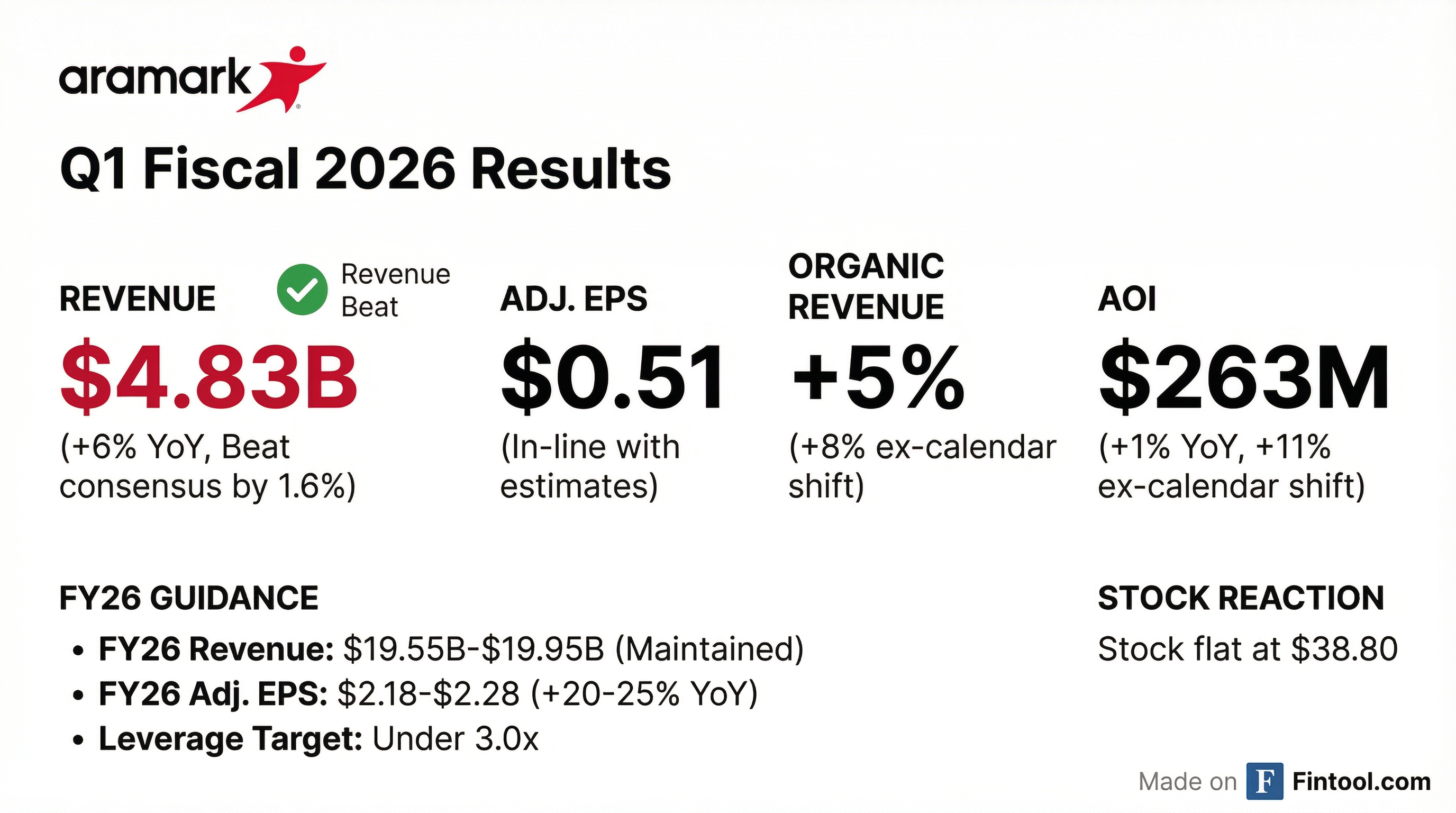

Aramark (NYSE: ARMK) reported Q1 fiscal 2026 results that beat revenue expectations despite a calendar headwind, while announcing RWJBarnabas Health—one of the largest healthcare contracts in recent history. Revenue of $4.83B topped consensus by 1.6%, driven by strong international growth and unprecedented client retention. Adjusted EPS of $0.51 matched expectations. Combined with the Penn Medicine launch completed last week, Aramark is adding roughly 10,000 hospital beds to its healthcare portfolio this fiscal year.

Did Aramark Beat Earnings?

Revenue: Beat by 1.6%

- Actual: $4,831.5M vs. Consensus: $4,756.2M

Adjusted EPS: In-line (+0.4%)

- Actual: $0.51 vs. Consensus: $0.508

The beat is more impressive when adjusting for a calendar shift caused by fiscal 2025's 53rd week. Without this timing headwind, organic revenue growth would have been approximately 8% (vs. reported 5%), and Adjusted EPS growth would have been +13% (vs. flat as reported).

What Changed From Last Quarter?

Positive developments:

- Revenue beat vs. miss streak: Q1 2026 marks Aramark's first revenue beat in 6 quarters, breaking a string of modest misses

- Net new business accelerating: "Certainly running ahead of where we expect it to be in terms of net new... well on track to deliver and perhaps exceed on the 4%-5%"

- Unprecedented client retention: "At a better spot in terms of retention this year than prior year" despite FY25 being a record year

- Debt repricing: Successfully repriced $2.4B of 2030 Term Loans, reducing interest rate by 25 basis points

- GLP-1 costs addressed: Medical cost program revamped, "no longer a factor starting January"

Headwinds:

- Calendar shift impact: The 53rd week in fiscal 2025 created a timing mismatch that reduced Q1 revenue by ~$125M (~3%) and AOI by ~$25M

- Elevated CapEx: Running at 4.5% of revenue (vs. historical 3.5%) due to new business in sports and higher-ed

How Did Each Segment Perform?

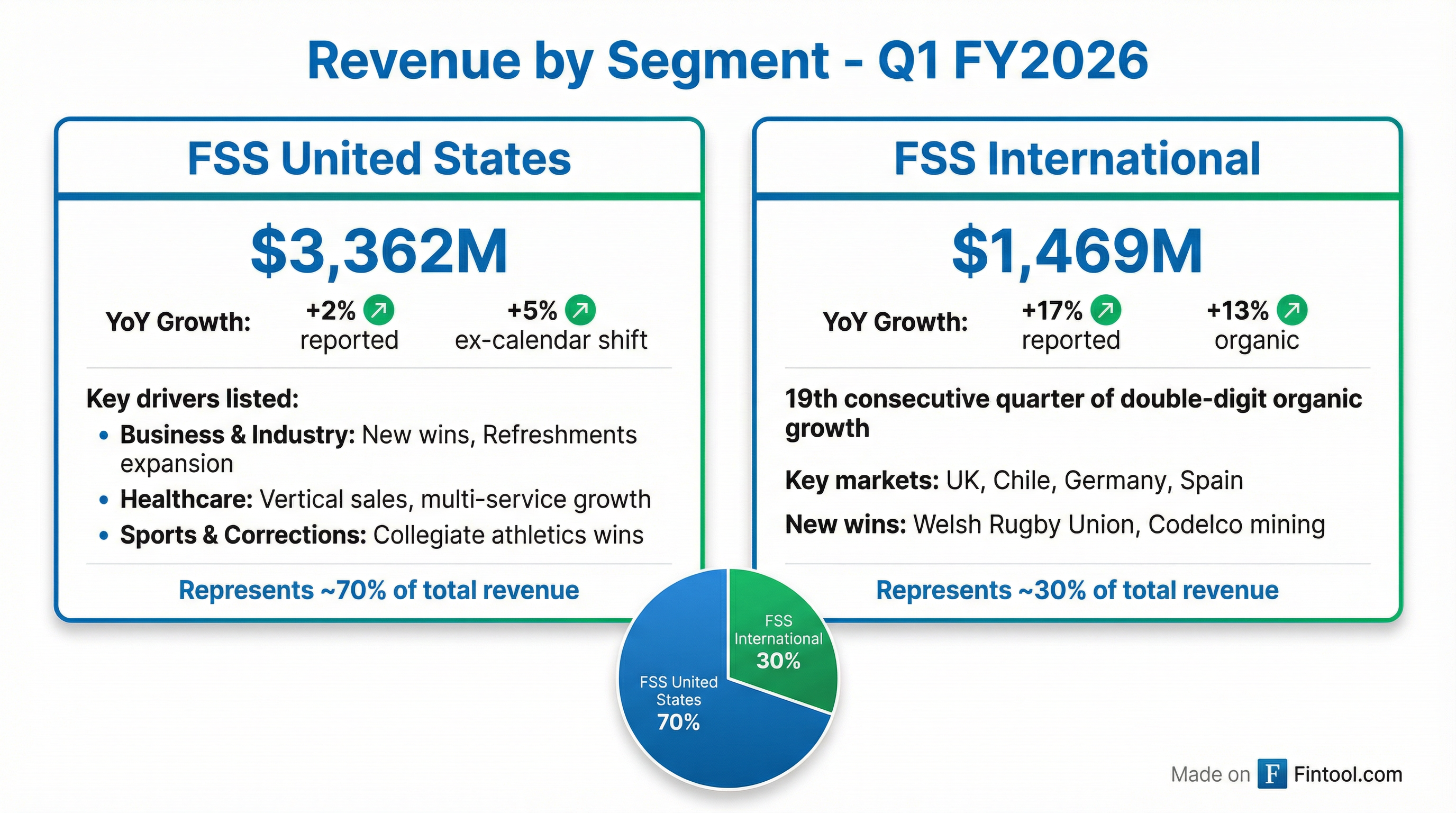

FSS United States ($3.36B, +2% YoY)

The US segment saw growth muted by the calendar shift, which reduced revenue by an estimated 3%. Excluding this impact, organic growth would have been ~5%.

Key drivers:

- Business & Industry: 17th consecutive quarter of double-digit organic growth, driven by new client wins and Refreshments account mobilization

- Healthcare: Blockbuster quarter for new wins (see below)

- Sports & Entertainment: Expanded college football portfolio with "pro-level hospitality experience"—alcohol unit sales now comparable to NFL stadiums

- Corrections: Added Alabama Department of Corrections (27 facilities statewide) with AI-integrated menu planning and operations

- Education: University at Albany and DePaul University operations commenced

What Major Contracts Did Aramark Win?

This was a transformational quarter for Aramark's healthcare business. Management announced two of the largest contract wins in the company's history:

Penn Medicine (Launched January 2026)

- Size: 4,000 beds across 7 hospitals

- Services: Patient and retail food service, environmental services, patient transportation, integrated call center

- Significance: Largest contract win ever in the US for Aramark

RWJBarnabas Health (Launching Summer 2026)

- Size: 5,700 beds across 18 primary locations

- Coverage: New Jersey's largest academic health system, serving 5M+ people across 8 counties

- Services: Patient and retail dining, environmental services, patient transport

- Significance: "One of the largest contracts awarded in healthcare in recent history"

- P&L impact: Material contribution expected in FY26 with ramp through summer; faster path to profitability than sports wins due to cost-plus structure

CEO Zillmer attributed the healthcare wins to a strategic shift by clients toward systemization:

"Penn Medicine had multiple service providers, and they were also self-operating a lot of their business. Their CEO made a very strategic decision to consolidate and systemize, so that they could capture the cost savings and the synergies, and ultimately to reduce costs to patients and control expenses... In a world of declining reimbursements from the federal government, they need to operate more efficiently."

FSS International ($1.47B, +17% YoY reported, +13% organic)

International delivered its 19th consecutive quarter of double-digit organic revenue growth, with every country contributing and results "largely unaffected by the calendar shift."

Notable wins:

- Welsh Rugby Union at Principality Stadium (74,000 capacity)—hosting Six Nations Rugby Championships

- Codelco copper mining contract in Chile (state-owned copper mining giant)

- Over 100 core account wins globally in Q1 alone

Geographic strength: UK, Spain, Germany, and Chile led growth

On Europe's sustained momentum, CEO Zillmer: "They've just done an extraordinary job of building that business over several years. They've been hyper-focused on growth... We've invested in sales, resources, processes and systems, and frankly, in leadership."

What Did Management Guide?

Aramark maintained all full-year FY2026 guidance:

*FY25 revenue on 52-week basis for comparison

Key modeling assumptions for FY26:

- Net interest expense: $315M - $325M

- Adjusted tax rate: ~26%

- Share count: ~270M

- Currency translation benefit: ~$100M to revenue

Calendar shift timing: The Q1 headwind is expected to reverse in Q2 and Q4, with 3-4 additional operating days benefiting those quarters.

What Did Management Say?

CEO John Zillmer emphasized unprecedented retention and the growth opportunity:

"We believe we're well positioned to record record-breaking financial performance, driven by our growth mindset, operational discipline, and unwavering commitment to service. We're seeing multiple positive growth trends throughout the organization, including extraordinary client retention in both FSS U.S. and International—levels we've never seen before achieved at this point in the fiscal calendar."

On retention and competitive positioning:

"We are at a better spot in terms of retention this year than prior year. And as you know, last year was a record retention for the organization... It's in early days, but I think we're on track to be consistent or even better than what we delivered in fiscal 2025."

On the consumer environment:

"We continue to see broad consumer support... We're seeing very good per capita spending, very good attendance levels in the various leagues. We're not seeing any consumer pushback or any strong concern with respect to the economic environment. Overall, I'd say it's steady as she goes."

CFO Jim Tarangelo on the outlook:

"We're off to a great start to fiscal 2026. The unprecedented levels of success with our annualized gross new wins and client retention last year have built the foundation for our strong outlook, and we believe we're well on track to deliver on our financial targets for 2026."

How Is Aramark Using AI?

Management highlighted AI as a key profitability driver, emphasizing minimal investment requirements:

"Our investment in AI is really relatively small. It is part of our normal IT operating budget. We don't have any significant program investment or significant capital investment targeted towards AI implementation. We're able to do this as part of our ongoing IT spend and driving significant performance improvement already through it."

AI-driven supply chain capabilities:

- Mobile AI chatbots for GPO clients

- AI-enhanced analytics providing "real-time visibility into their business"

- Back-end systems "accelerating back-end efficiency and productivity gains"

- AI platforms for menu planning (deployed at Alabama DOC across 27 facilities)

On AI as opportunity vs. threat:

"The vast majority of our businesses will probably see an opportunity coming from the application of AI in their respective segments. We don't see it as a threat to the business. We see it as an opportunity for further growth. Obviously, if data centers are under construction, we would certainly have an opportunity to pursue and bid on those kinds of opportunities. It's very analogous to our remote camps and mining businesses."

How Did the Stock React?

ARMK shares were essentially flat following the release, trading at $38.80 (+0.2%). The muted reaction reflects:

- Results largely in-line with expectations

- Calendar shift dynamics were well-telegraphed

- Maintained (not raised) guidance

- Stock had already recovered from Q4 FY25 miss

Valuation context:

- Current price: $38.80

- 52-week range: $29.92 - $44.49

- Market cap: ~$10.2B

- Trading near 50-day MA ($38.08) and below 200-day MA ($39.04)

Capital Allocation Update

Aramark continued executing its balanced capital allocation strategy:

Q1 Actions:

- Share repurchases: $30M bought back

- Dividend: $0.12/share quarterly (increased 14% in November 2025)

- Debt management: Repriced $2.4B of 2030 Term Loans by 25 bps

Balance sheet:

- Cash availability: ~$1.4B at quarter-end

- Net debt: $5.8B

- Net debt / Covenant Adjusted EBITDA: 3.9x (target: under 3.0x by fiscal year-end)

- No significant maturities until fiscal 2028

Q&A Highlights: What Did Analysts Ask?

Organic Growth Components (Full Year)

CFO Jim Tarangelo provided the FY26 algorithm breakdown:

- Pricing: ~3% (in line with inflation)

- Volume: 0.5% - 1%

- Net new business: ~4.5% (tracking to potentially exceed 4-5% target)

Competitive Wins Strategy

On taking business from competitors and self-op conversions:

"We've been lucky enough to win two very large opportunities in Penn and RWJBarnabas, that represent very significant both competitive wins and self-op conversions. We're positioned extraordinarily well to win in these situations. The capabilities our teams have built, the systems we can bring to bear... are significant."

Inflation Update

CEO Zillmer on cost environment:

- Food inflation: ~3% globally, "right in that range of what we anticipated"

- Labor costs: Similar ~3% range

- Beef specifically: Demand outstrips supply, but mitigated through menu design

- Overall: "Nothing extraordinary in the inflation environment at this stage"

GLP-1/Medical Costs

The company addressed elevated medical costs from GLP-1 drugs mentioned last quarter:

- Program has been "revamped"

- No longer a factor starting January 2026

CapEx Normalization

CFO on capital intensity:

- Q1 CapEx: 4.5% of revenue (elevated)

- Historical run rate: ~3.5%

- Expect normalization by year-end

- Elevation driven by sports and higher-ed new business (higher capital intensity)

World Cup 2026 Impact

On the FIFA World Cup games at Aramark-operated stadiums:

- Will operate games at Lincoln Financial Field (Philadelphia), NRG Stadium (Houston), and Kansas City

- Net impact: "Relatively revenue and profit neutral"

- Reason: Games displace concert activity and other events typically held during that period

Key Risks and Concerns

Near-term risks flagged in the release:

- Tariff exposure from US trade policies

- Multiemployer pension plan withdrawal charges ($5.6M in Q1)

- Hyperinflation in Argentina (modest impact)

- Antitrust review legal costs ($1.3M in Q1)

Seasonal cash flow: Q1 typically shows significant cash outflow due to business seasonality (collegiate, sports, destinations). This normalizes by Q4.

What to Watch Going Forward

- RWJBarnabas launch (Summer 2026): Implementation schedule still being finalized; will have "significant impact in 2026" starting June

- Q2 calendar benefit: The timing shift should boost Q2 results by ~3% to revenue, making it a better indicator of underlying momentum

- Net new business trajectory: Management is tracking ahead of 4-5% target with "very robust pipeline of opportunities, many active discussions and many of those pretty close to finalizing"

- Healthcare consolidation pipeline: Management hinted at "other large pursuits ongoing" but declined to detail due to competitive sensitivity

- International momentum: 19 consecutive quarters of double-digit growth—any deceleration would be notable

- Seattle Seahawks Super Bowl win: Aramark serves Lumen Field facilities; should benefit from championship-related events

Data sourced from Aramark Q1 FY2026 earnings release, earnings call transcript (February 10, 2026), and S&P Global.